Regular Income Bonds: A Pro Guide to Steady Returns and Smart Investing,

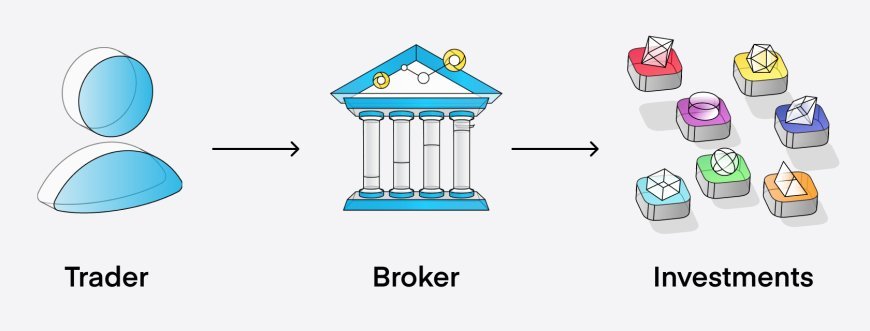

In a world where market volatility can turn a portfolio’s value upside down in weeks, investors often crave stability and predictability. Regular income bonds fixed-income securities that pay interest periodically offer exactly that: a consistent stream of cash flow without the roller-coaster ride of equities.

But while they seem straightforward, the real magic happens when you apply professional strategies to maximize their benefits.

Continue reading this piece by saajan

Join our community to access the full story. Creating an account is completely free and only takes a moment.

- Read unlimited free publications across the platform

- Directly support independent journalists and authors

- Join discussions, leave reactions, and save your favorites

Responses (0)

Sign in to share your thoughts.

Sign in